Commerce Report Switzerland 2022: Management Summary

Values and services in the focus of trade.

Management Summary of the Commerce Report Switzerland2022

The Commerce Report Switzerland is a series of studies started in 2009. It examines with the influence of digitalisation on the development of industry structures and business models for the sale of products and services to private consumers. This 15th report is the result of a comprehensive survey in spring 2022 of 32 potentially market-defining e-commerce and multichannel providers in Switzerland. The results are mainly derived from the statements of the experts on the study panel.

2021 – the second exceptional year of covid-19

In 2021, the second year of covid, Swiss retail as a whole experienced a third record year in a row with an increase of 3.2%. For the first time, it exceeded the 100 billion franc mark. Taking e-commerce sales under the .ch domain into account, the figure of CHF 90 billion is only on par with 2011, ten years earlier. Overall, e-commerce grew by 9.9% to CHF 14.4 billion in 2021. This roughly corresponds to the growth rates of the three years prior to the pandemic. With online growth of 27%, 2020 is proving to be a unique e-commerce booster year. The share of foreign online providers stagnated in 2021, meaning that their market share fell for the third year in a row.

Start of 2022 – entering the new normal

The sales figures for the first half of 2022 are now available: at GfK Markt Monitor Schweiz, the data from a panel of 60 significant companies showed a decline of 5.7% compared with the first half of 2021. The Swiss Distance Selling Market Monitor, which is based on around 100 registered providers, reports a decline of 6.1%. When evaluating these figures, it must be remembered that there was a lockdown in the first half of 2021. Compared with the first half of 2019, the 2022 figure for the overall market was about 5% up, and a whopping 47% in the case of e-commerce. In the long-term comparison, the level remains very high.

The fact that normalisation would initially begin with a setback came as no surprise to many study participants. So far as e-commerce is concerned in 2022 as a whole, a clear majority is expecting growth again.

Change of era and outlook until 2030

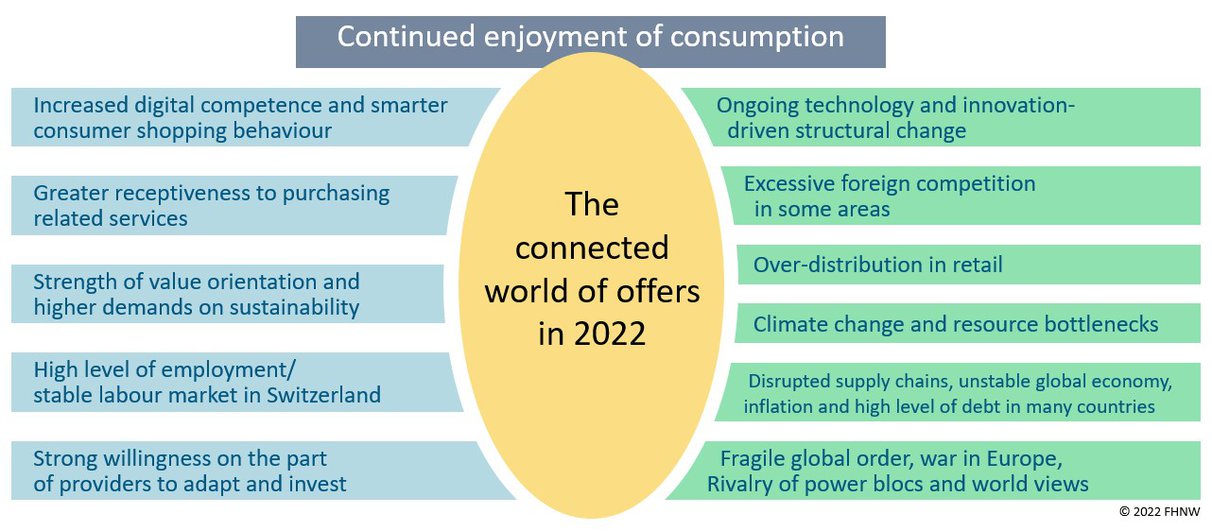

The pandemic was a turning point for the whole of humanity. In the consumer goods industry, it marked a change of era: the traditional debate about brick-and-mortar versus online has vanished. For consumers, it is about getting the maximum benefit in the connected world of offerings. Whereas for providers it is about adapting positioning, perhaps even about surviving. Structural change has crept in over the years and is now accelerating. This study report attempts to outline what impact this could have in a near-term perspective until 2024 and in a longer period until 2030 – under stable economic conditions. Fig. 1 provides an overview of the currently most important circumstances.

Within the sector, there are three main trends that are changing the industry:

- The advancing, technology-driven dissolution of traditional role models has led to over-distribution, particularly in retail, which is forcing many providers to reorient themselves.

- Direct sales of brands and manufacturers have become normal and require more closely coordinated, and also a better-paid, cooperation with retailers.

- Digital platforms are continuing to expand their role in consumer goods distribution.

In addition, there are external factors, including the stronger value orientation of customers, employees and the public, and the likely prolonged upheavals in the global division of labour in production and logistics.

Fig. 1: The general conditions for sales to consumers in 2022

Despite increasing consolidation, the world of supply could be even more diverse in 2030 than it is today. Digitalisation is facilitating success in niche segments that meet increased value- and service-oriented demand. The goods themselves will be more expensive than they are today. Probably fewer will be purchased, but they will be more valuable. Two tasks are gaining in importance for providers: operating the business on behalf of consumers with a contemporary approach to value and combining sales with needs-oriented services.

Retail is focusing on values and service.

Assessment of the situation after two years of COVID

Both Swiss retail as a whole and e-commerce will remember both 2020 and 2021, which were shaped by the COVID-19 pandemic, as extremely challenging years. However, the two-year period was exceptionally strong in terms of sales from a cross-industry perspective. The exceptional economic situation will end though in 2022: consumers are spending more on travel, food and experiences, leaving less for consumer goods. But in the long term, the qualitative changes brought to the market by COVID will become more important. They would probably also survive an economic slump, which is not expected but cannot be ruled out in 2022.

By a large majority, the study participants confirmed the characteristics underlying the interpretation of a change of era in the last issue of the study: consumers have made a huge leap in mastery when using digital services for their purchases. They do not want to do without them now, even after the coronavirus pandemic. Day-to-day operations are also more flexible thanks to the permanently more flexible forms of work – they have resulted in more diverse purchasing requirements. Depending on the situation, customers sometimes choose a stationary channel, other times an online channel, and combine these smartly within a single shopping process if it proves the most useful for them.

Apart from the increased competence, the increased expectations of sustainable and value-oriented trading are considered to be the most significant change among consumers. However, the trend is not only related to consumption, since employers also have to address the issue. Psychology helps show why most people reveal mismatches between their beliefs and behaviours.

The importance of the change of era for providers

Most providers have quickly recognised the change in era, are investing, and are now working hard on expanding their digital expertise. Laggards also want to be digitally accessible and be able to interact with their customers. This will also require increasing digitalisation in the companies themselves: more and more work is being done to set up basic functions in the form of automatable, digitalised services for internal and external users.

But the most important prerequisite for success during the structural change occurring in the currently particularly dynamic world is the mindset as well as the approaches of companies as they develop and advance their positioning. It is therefore less important whether a company was originally primarily focused on bricksand-mortar or online. Seven paradigms that characterise mindset have been identified and made clearer in the interviews. They begin with access to customers, they address the importance of thinking in digital services, and they see a need for continuous improvement and innovation. Finally, the company’s own organisation is addressed at four levels, from cooperating in external partnerships to employees. The importance of the employees and their ability to survive in the given dynamic is seen by the study participants as the most important success factor.

Over-distribution, displacement and consolidation

At the heart of this series of studies is the development of distribution to consumers under the influence of digitalisation. Reflecting on the development of recent years, it is noticeable that the size and variety of the range of products on offer to consumers has continued to increase, as has competitive pressure among suppliers. The reason for this is rampant over-distribution. This is due to the reach of the Internet and has experienced another boost with the change of era. Whereas brick-and-mortar stores only serve a regional audience, a single Galaxus website is open to all potential department store and specialist retail customers. A single online provider can replace countless retail outlets, but only as long as it can attract customers its channel. Conversely, a bricks-and-mortar retailer may have the advantage of being the only provider with a retail outlet in its region, while Galaxus is always in competition with all other online providers. Over-distribution means that there are too many offers across channels that do not differ significantly from the customer’s perspective. This usually leads to a fierce price war. Fewer of these offers are needed, which means fewer shops and online shops.

This is not good news for individual providers, whether they are traditional or primarily online, as the question about supplier concentration did not produce any positive results either: 80% of respondents expect consolidation to continue. It is increasing in many industries with comparatively few online marketplaces and strong online shops in conjunction with Google and other players that are important for access to customers.

Diverse purchasing needs

On the other hand, the study participants also expect a diverse world of offerings in a horizon up to 2030. Besides a few very large providers and marketplaces, many small, focused, or regional product and service providers are also anticipated to have a place here. What can this variety bring about? A starting point for the answer is the finding that customer value orientation has increased and openness to services related to purchases has gone up. Accordingly, more variety could arise from the fact that retail, which is largely geared towards physical product distribution, is focusing more strongly on value orientation and needsoriented services. This is at the heart of the traditional self-image of retail, but is intended to go beyond the logistical functions of retail!

Value- and service-oriented market segments

To differentiate between the market segments derived from the value- and service-oriented demand, the market was mentally divided into two segments, although in practice these cannot be differentiated. Segment 1 stands for the traditional consumer goods market, which is primarily functionally geared towards the products themselves. This represents today’s international market for mass industrial products, where supplier consolidation is increasing and economies of scale are one of the most important factors for success. Segment 2 stands for a primarily value and service-oriented market segment in which the product is only part of an overarching service. Compared with a product from segment 1, this service contains an additional service component that is decisive for buyers. The additional service component can be based on a product from segment 1 as a service, for example as a fast delivery service for foods that are spontaneously needed.

Diverse potential for differentiation

Segment 2 offers need differentiators that make the difference for buyers to purchase higher than the lowest price. The report covers many different examples of opportunities for differentiation. One group covers opportunities that tie in with the identity of the target customers, such as lifestyle offers. A second group is about value-oriented product and range features, as there are many options for product-service combinations. The latter are tailored towards the convenience of the shopping, to a specific customer situation, or to leisure-shopping combinations. A short commentary deals with the much-discussed topic of quick commerce.

Segment 2 offers opportunities for providers who are forced to reorient themselves due to over-distribution. With some providers, segment 2 is already quite well developed, at least in some areas. However, the services are often only seen as an ancillary service. Many suppliers find it difficult to rethink from product to overarching value or service.

It is obvious that the economic potential of many areas in segment 2 boils down to niche segments, a mass of niches. This does not mean that they would be reserved for small providers: combined with the cost benefits of bulk business, they can also provide promising diversification for large companies.

Provided that the general social and economic conditions in Switzerland remain stable, the study participants expect an increasing market share for offers geared towards value and service-oriented demand segments. A quarter of participants can even imagine a market share gain of 20% by 2030 at the expense of the price-focused segment.

In addition, there are other drivers for the diversity of the future world of supply. These include the brands’ direct sales channels and social media platforms, which communicate offers to prospects in their own unique way.

New distribution with the customers at the centre

Traditionally, distribution is viewed as a linear chain. This has long ceased to mirror reality. The traditional role models have dissipated in the structural transformation and numerous new paths have emerged to divide up value creation among several participants. Another deficiency of the traditional image is that digital platforms do not appear in it at all, even though they play an important role today.

The large variety of constellations has resulted in competition between distribution systems in addition to competition between the individual companies. Which concept is superior – the split distribution chain or the vertically integrated provider?

During the course of the study series, a new picture of distribution has emerged which focuses on customers and represents the most important real and digital players. This picture serves as a starting point for discussing the different roles and the most important developments with regard to future development.

Every channel has its challenges

What concerns a lot of people is the future of brick-and-mortar retail. It is plagued by a plethora of trends that will continue to erode its importance in the coming years. The over-distribution that threatens many businesses has already been mentioned. However, this does not represent a general verdict against retail stores. There will still be large numbers of brick-and-mortar stores in 2030, especially local supply formats for everybodys daily needs. There are only certain combinations of operating models and locations that will work, and others that will gradually disappear. The retail business is no longer the focus of consumer goods sales. It still represents an important touchpoint, but one amongst many. This also applies to inner cities, which in the past were mainly populated by people who shopped at the local businesses. These are also now trying to reinvent themselves. Proximity still remains a strong argument. But who else wants to ride a bike to the city only to find out that what they are looking for is not available? Public spaces, as places where people like to be and where things are happening, have never been in greater demand. Leisure and consumption are closely linked, while experience and inspiration with all the senses will still prove far superior to digital experiences. Each location must find and maintain its own identity.

Traditional retail has been trying to connect to the online retail world with omnichannel concepts for around 15 years now. Despite massive efforts and selective successes, many concepts are unlikely to exist in their existing form by 2030. We have not yet found out what customers will really perceive as added value, and what will generate sufficient revenue at the same time. With low margins, a trading margin alone

is becoming less and less a justification for the huge efforts expended.

Online-only providers find it easier to adapt to rapid market changes. Their biggest challenges are gaining access to customers at sustainable costs, and the competition with large online marketplaces. The latter play a more or less dominant role, depending on the sector. Many people are certain that they will

continue to gain market share in the coming years.

A lot of movement is going on with customer access providers, especially among social media platforms. They stand at the threshold of the retail transaction. Many are wondering whether these platforms will remain true to their original role, keeping people’s exchanges with each other, and keeping the providers in focus. This is because values, culture and services that companies would like to differentiate themselves from can barely be represented on marketplaces. Other platforms are needed to live up to the old vision from 1999: Markets are conversations.

Click on study archive to obtain the complete study 2022 as well as all past reports for free.

Table of contents of the study 2022

Editorial on the 15th and final edition of the study series

Part 1: assessment of the situation

1 Review of 2021, outlook and trends from 2022 up to 2024

1.1 Numbers-based assessment of the situation for the industry

- Exceptionally successful years in terms of sales

- Recent years in terms of structural change

- Top 30 online stores: increasing concentration, capable of playing catch-up

1.2 How the companies in the 2021 study panel fared

- Looking back, there were mostly positive assessments for 2021

- What kept companies particularly busy in 2021

- Sales performance of the members of the study panel

1.3 Expectations for 2022 and up to 2024

- Industry expectations

- Expectations for the participants' own company in the current year 2022

- Expectations for foreign vendors

1.4 Three thesis on the permanent effects of the pandemic

- Thesis 1: more flexible daily routines, greater variety of purchasing needs

- Thesis 2: new receptiveness to services and stable price sensitivity

- Digression into psychology: Zalando's cry of happiness for free delivery

- Thesis 3: comeback of neighbourhood stores, only permanently reduced

1.5 Current trends put to the test

- Thesis 4: value-oriented action is now a must

- Thesis 5: online vendors with stores are more than an exception

- Thesis 6: stationary stores as hubs for deliveries – fairly unlikely

2 Digression: the Swiss Marketplace Group - a major coup!

Part 2: change of epoch and greater variety of products

3 Characteristics of the 2020 change of epoch

3.1 Consumers' new attitude

3.2 The new attitude of companies

- Be accessible to customers and able to interact with them

- Creating basic functions digitally and automatically

3.3 The right mindset as a success factor

- Seven paradigms of successful vendors

- Classification of the right mindset as a success factor

4 Intensified competition and necessary differentiation

4.1 Rampant overdistribution and persistent concentration

4.2 Need for differentiation

4.3 Differentiation through resonance with target customers

4.4 Differentiation through product features

- Value-oriented product features

- Non-commodity products and long-tail products

- Products from topic-focused vendors

4.5 Differentiation through product-service bundles

- Services that increase the convenience of shopping

- Quick commerce

- Services tailored to the specific customer situation

- Leisure/shopping combinations

5 More than products:: Value orientation and services

5.1 Value and service-oriented demand

5.2 Small and large vendors

6 Upshot: the future will bring a more diverse world of commerce

Advertorial: Feel-good Connected Commerce

Part 3: Status quo and outlook for the future

7 The image of distribution with the consumers at the centre

7.1 Traditional roles in the chain from manufacturer to customer

- The consumers ①

- The linear distribution chain and its roles ②

- Value-added functions of retail

- Alternatives in the organisation of distribution③ ④ ⑤ ⑥ ⑦ ⑧

7.2 Three retail business models

- The situation of stationary retail

- Cross-channel business concepts

- The situation of individual, pure e-commerce vendors

7.3 Close to the customers: the new roles in the network

- Customer access service providers⑨

- Online marketplaces ⑩ ⑪

- Local logistics supply ⑫

7.4 Brands and manufacturers versus retail

- Changes to the market from a brand perspective

- The retail perspective

- Upshot: competition in distribution systems

8 Expectations in an outlook up to 2030

8.1 Continued growth in e-commerce market share

8.2 Impact of long-term trends on the industry

9 Study design

Authors

Comments and sources